Emerging markets (EM) have long been a strategic allocation within Frontier’s global equity configuration advice to clients, offering diversification, higher growth potential and the prospect of enhanced long‑term returns. Yet for much of the past decade, the asset class has failed to live up to expectations, persistently underperforming developed markets (DM) and testing investor conviction.

After a year of outperformance in 2025, an important question has re‑emerged: Is this another false dawn, or has the investment case for emerging markets genuinely strengthened?

In this paper, we revisit the original rationale for a strategic allocation to EM and consider what has changed. We examine whether the assumptions underpinning long‑term allocations still hold, assess improvements in fundamentals, and explore the evolving role EM can play in portfolios today. We also outline key risks and implementation considerations investors need to keep front of mind.

Why emerging markets remain strategically important

We have consistently supported a dedicated allocation to emerging markets within global equity portfolios. Historically, this view has been grounded in four key arguments:

- Diversification benefits for Australian investors, particularly given high domestic equity exposure.

- Underrepresentation in global benchmarks, relative to EM’s contribution to global GDP.

- Stronger long‑term growth potential, underpinned by favourable demographics and rising productivity.

- Potential for enhanced risk‑adjusted returns, especially over long investment horizons.

These arguments remain broadly intact today. In fact, some have strengthened.

While EM equity performance has lagged developed markets since 2010, recent years have seen a meaningful shift, in our view. Correlations between EM and Australian equities have declined, improving diversification outcomes. Active managers in EM have continued to generate excess returns relative to their developed market peers. And after a prolonged period of disappointment, earnings growth in EM is showing signs of life.

A possible turning point for EM performance

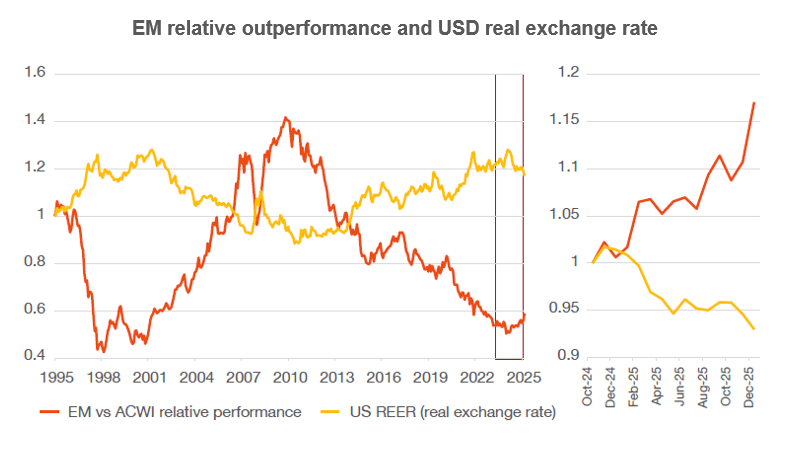

The past 15 years have been challenging for EM investors. A slowing Chinese economy, persistent US dollar strength and a powerful technology‑led rally in DM amalgamated to drive sustained underperformance.

Periods of EM recovery did occur along the way, in 2016–17, and again around 2019–20, but ultimately proved to be short‑lived. As a result, scepticism around any renewed EM outperformance is understandable. However, the rebound in 2025 looks different in several respects.

EM outperformance has broadened across regions rather than being driven by a single country or factor. Performance leadership has rotated between Emerging Europe, Korea, Taiwan, China, South Africa and Latin America, highlighting the increasing breadth of the asset class. At the same time, EM returns have been supported by improving fundamentals rather than purely cyclical tailwinds.

Whether this marks the start of a sustained period of relative outperformance remains uncertain, but we remain constructive that we are seeing genuine structural change.

Improving fundamentals across emerging markets

Stronger policy frameworks

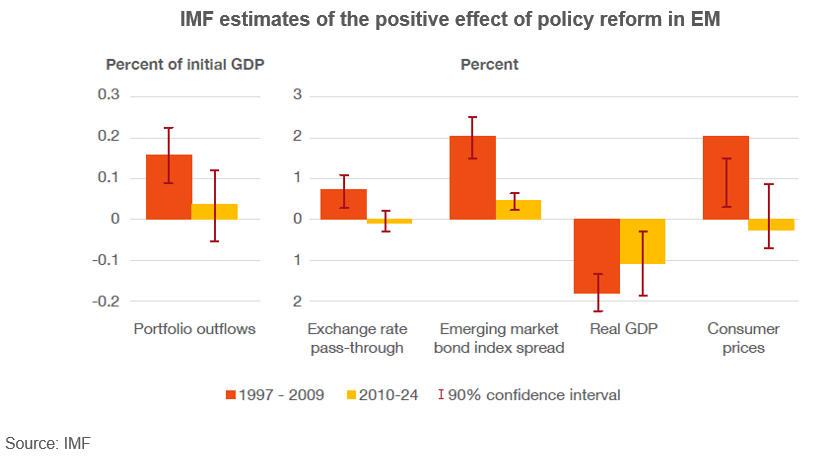

One of the most notable developments across emerging markets over the past decade has been the strengthening of monetary, fiscal and macro‑prudential policy frameworks.

Many EM central banks now operate explicit inflation‑targeting regimes, public debt burdens are often lower than in developed markets, and reliance on foreign‑currency borrowing has declined. Local currency financing markets have deepened, improving resilience to global financial shocks.

The result is emerging economies today tend to experience smaller output losses and more contained inflation during periods of global stress than they did historically. For equity investors, this translates into a more stable operating environment and a potentially improved risk‑return profile over the long term.

Corporate governance reform gathering pace

Top‑down policy improvements are increasingly being matched by progress at the corporate level.

A number of large EM economies have launched governance initiatives aimed at lifting capital efficiency, shareholder returns and transparency. Korea’s Corporate Value‑Up Program, China’s market‑value management reforms and Brazil’s adoption of international sustainability reporting standards all highlight a growing focus on shareholder alignment.

While it is still early days, these initiatives are starting to address a long‑standing weakness in EM, the failure of economic growth to translate into corporate earnings and investor returns.

Earnings growth showing early momentum

Despite strong GDP growth historically, EM company earnings stagnated for much of the past decade. Dilution, weak governance, falling returns on equity and US dollar strength all weighed on performance.

More recently, this has begun to change. Improved governance, greater discipline around capital allocation and more favourable macro conditions are contributing to a recovery in earnings growth across EM. While not yet definitive, the trajectory is encouraging, and critical to the long‑term investment thesis.

Resilience in a more fragmented global economy

Trade tensions and tariff risks have traditionally been a major headwind for emerging markets. Yet the experience of 2025 suggests EM economies are now better positioned to absorb these shocks.

A key structural shift has been the growth of South–South trade, with emerging economies increasingly trading with one another rather than relying solely on developed markets. This trend has been building for decades and has reduced EM dependence on the US and Europe at the margin.

China provides a useful case study. Despite elevated tariffs, growth has been supported by exports in higher‑value sectors such as autos, semiconductors and advanced manufacturing. Regional integration and diversification of trade partners have helped cushion the impact of geopolitical uncertainty.

This rising resilience strengthens the case for EM as a strategic, rather than purely cyclical, allocation.

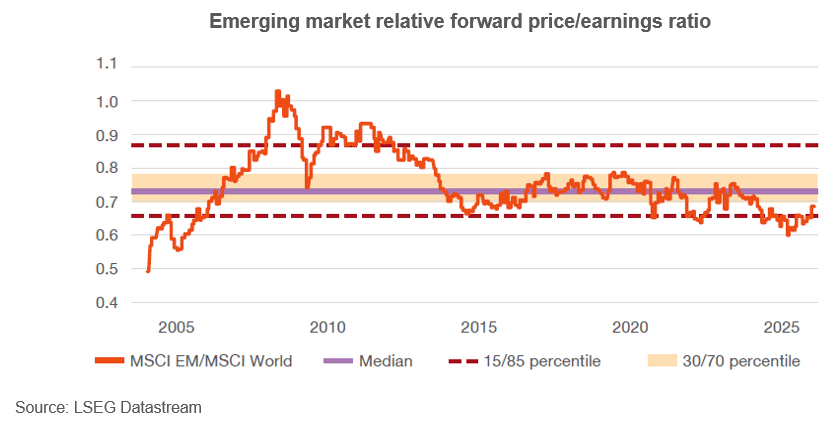

Valuations: relative appeal remains

From a valuation perspective, EM does not look cheap in absolute terms. However, relative to developed markets, particularly the US, valuations remain more reasonable.

The discount between EM and DM has narrowed but remains supportive, especially in the context of improved fundamentals. Much of the valuation gap reflects elevated multiples in developed markets rather than depressed EM pricing.

For investors looking to increase or establish an allocation, EM currently offers a relatively attractive entry point.

An evolving ESG profile

Emerging markets continue to carry elevated ESG risks, particularly around governance, labour standards and regulatory consistency. These risks should not be understated.

That said, the overall ESG profile of EM has improved meaningfully. Governance reforms, improved disclosure standards and a growing role in the global energy transition are reshaping perceptions.

Notably, several emerging economies (led by China), are now major investors in clean energy, electrification and decarbonisation technologies. As renewable technologies become increasingly cost‑competitive, EM countries are playing a central role in scaling global solutions.

For long‑term investors, this evolution adds another dimension to the improving fundamental picture.

A powerful source of diversification today

US dollar exposure and portfolio balance

One of the most compelling arguments for EM today lies in diversification, particularly against US dollar risk.

Australian institutional portfolios are more exposed to foreign currency, and to the US dollar specifically, than at any point in recent decades. Historically, periods of US dollar weakness have been associated with EM outperformance, through improved balance sheets, stronger domestic demand and rising commodity prices.

With the US dollar cycle now long in the tooth, EM equities offer meaningful diversification benefits should conditions shift.

Diversifying AI exposure

Developed market equity benchmarks are increasingly concentrated in a narrow group of US technology and AI‑exposed stocks. These companies dominate cloud infrastructure and model development, leaving portfolios vulnerable to style, sector and valuation risk.

Emerging markets offer a complementary form of AI exposure, with greater emphasis on applications, hardware, semiconductors and enabling ecosystems. While headline index weights can appear concentrated, underlying correlations with US mega‑cap technology stocks are far lower than many investors assume.

In this way, EM can help diversify both traditional equity risk and thematic exposure to AI.

Risks and implementation considerations

Despite improving fundamentals, EM remains inherently more volatile than developed markets. Political intervention, regulatory change and geopolitical events can occur with little warning and can lead to sharp drawdowns.

These risks reinforce the case for:

- A strategic, long‑term approach, rather than tactical allocation.

- Active management, to navigate country‑specific risks and exploit inefficiencies.

- Thoughtful portfolio construction, including consideration of EM ex‑China or standalone country allocations where appropriate.

There is no one‑size‑fits‑all approach. Investors must weigh complexity, governance capacity, tracking error tolerance and existing look‑through exposures when determining how best to access EM.

The final word

Emerging markets have spent much of the past decade testing investor patience. Yet the asset class entering 2026 looks fundamentally different from the EM of the early 2010s.

Stronger policy frameworks, improving governance, renewed earnings momentum and enhanced diversification characteristics suggest the long‑term case remains intact, and arguably stronger than it has been for some time.

While risks remain, emerging markets continue to offer:

- Diversification in an increasingly concentrated global equity landscape

- Exposure to faster‑growing economies

- Improving fundamentals and governance

- Attractive relative valuations

- A complementary pathway to key structural themes such as AI and decarbonisation

For long‑term investors, now is an appropriate time to reassess whether their exposure to emerging markets remains fit for purpose. Get in touch with us if you would like to learn more.

Clients can access the comprehensive paper on Frontier Partners Platform.