Australian unregulated, long‑tail liability investors play a critical role in providing insurance coverage across compulsory third‑party, workers compensation and other government‑backed schemes. These investors typically manage long duration liabilities that might grow faster than inflation, making investment outcomes a key driver of long‑term sustainability. Unlike regulated insurers, these schemes generally operate with greater investment flexibility and longer time horizons, allowing portfolios to be structured differently in pursuit of real returns.

Due to this greater flexibility, unregulated investors typically take on higher levels of investment risk. This is reflected in their portfolios which tend to hold a larger allocation to growth assets relative to defensive assets. Over recent years, we have observed a consistent shift away from traditional defensive assets towards ‘mid‑risk’ assets such as unlisted infrastructure, unlisted property and private credit. These assets are attractive due to their ability to deliver diversification beyond equities and bonds, reduce return volatility and provide more stable income streams.

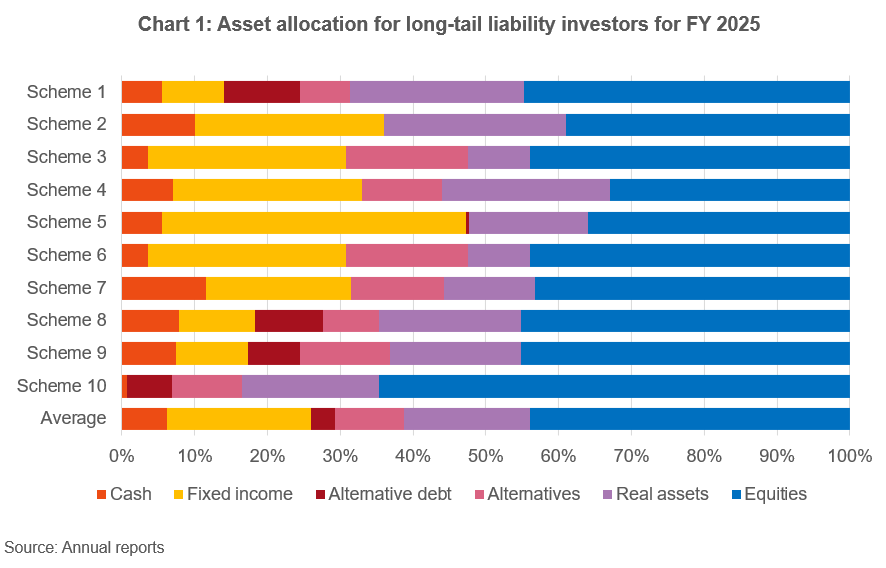

Chart 1 illustrates the asset allocation of long‑tail liability investors in FY25, highlighting the high allocations to equities and real assets across the cohort. This analysis is based on publicly available data for the schemes, mainly via annual reports, and is dependent on the level of detail included. For example, there may be differences in the exact nature of the underlying assets classified as ‘Alternatives’.

With higher risk appetite comes higher allocation to risky assets and hence flexibility to aim for a higher return objective. It is important to highlight the relationship between growth allocation and return objectives. In practice, investment strategy is not defined by the risk-return trade-off alone but a trilemma between solvency, risk and return. While higher growth exposure can improve the probability of achieving long‑term return objectives, funding position and solvency buffer play a critical role in determining how much risk a scheme can sustainably take.

Long‑tail liabilities are highly sensitive to both interest rate and inflation movements. To remain sustainable, portfolios must be able to:

- Remain solvent and ideally maintain a funding ratio within their preferred target range.

- Generate a sustainable real return over long time horizons, growing assets ahead of liabilities.

- Absorb short‑term market volatility.

- Demonstrate resilience through economic cycles.

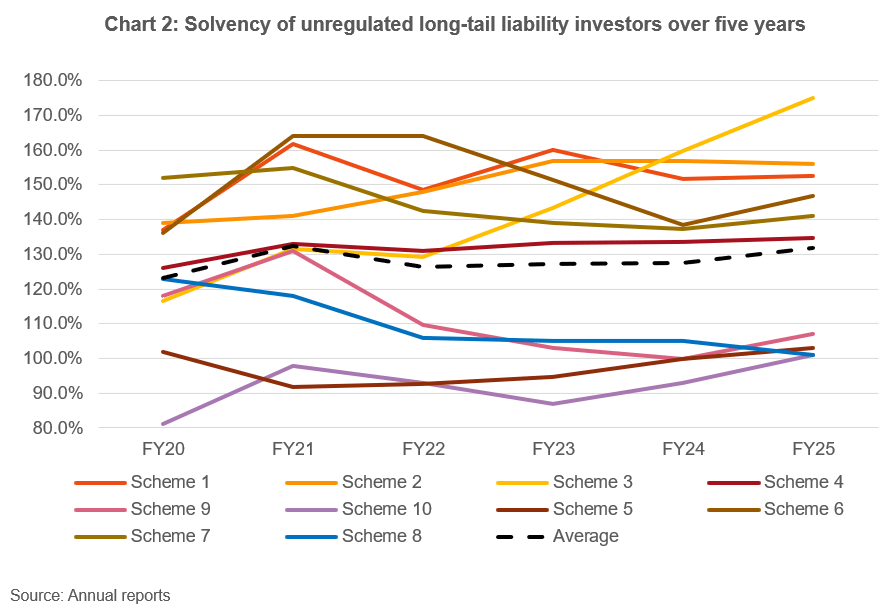

As mentioned, the key aim of the long-tail liability investors is to maintain funding ratios within target ranges and to achieve investment return objectives that exceed liability growth. Chart 2 shows most schemes have maintained or improved their solvency level over time underpinned by strong asset returns and increased asset valuations.

Ultimately, the 2025 financial year has been a stable and positive period for unregulated schemes. Investment performance remained strong, supported by strong returns from equities and real assets. Moreover, moves toward mid-risk and growth assets over the years have positioned these investors to continue meeting long-term objectives.

However, as we are moving to a more normalised environment where traditional income producing, defensive assets look more attractive, are we starting to see a shift back towards a more defensive setting?

Our team has prepared a detailed analysis of the key trends within long-tail liability investors over five years using their respective annual reports. Get in touch with Frontier’s LDI and Government Team for more information and insights.